As the clock ticks towards 2026, the impending expiration of the Tax Cuts and Jobs Act (TCJA) looms over us, promising significant changes to the tax landscape. This shift has many individual taxpayers to large corporations and business owners scrambling to find strategies to mitigate its impact.

Why should this matter to you? The TCJA, implemented in 2017, brought about sweeping changes to the U.S. tax code, impacting deductions, exemptions, and tax rates across the board. Its expiration means a potential increase in tax liabilities for many, making financial planning more critical than ever.

But fear not! This guide will unveil seven tax hacks that are intended to not only to help you navigate these changes but to thrive, turning potential challenges into opportunities. Whether you’re an individual looking to optimize your tax situation or a business aiming to maintain its competitive edge, these strategies will provide invaluable insights.

Keep reading to uncover the secrets to understanding the 2026 tax hike implications, ensuring your financial planning is both proactive and powerful.

Roth Conversions

The sunset of the TCJA brings a unique opportunity for Roth IRA conversions. With the potential increase in income tax rates post-2026, converting your traditional IRA into a Roth IRA now could save you a significant amount in taxes over the long term. This move is especially advantageous if you expect to be in a higher tax bracket in the future or if you’re looking to provide tax-free income to your heirs.

By paying taxes on your retirement savings now, at potentially lower rates, you can enjoy tax-free withdrawals later. This strategy not only hedges against future tax rate increases but also eliminates Required Minimum Distributions (RMDs), offering a more flexible and tax-efficient retirement income strategy.

Federal Lifetime Gift and Estate Tax Exemptions

One of the most compelling aspects of the TCJA is the doubled federal lifetime gift and estate tax exemptions, which are set to revert to their pre-TCJA levels after 2025. This presents a golden window for estate planning, allowing individuals and families to transfer significant wealth to their heirs with reduced tax implications.

Taking advantage of these higher exemptions now can mean massive tax savings for your estate and a more substantial inheritance for your beneficiaries. One way to maximize this opportunity is through the estate planning strategy of creating trusts or making strategic gifts.

State and Local Tax Deduction (SALT) Limitations

The TCJA capped the SALT deduction at $10,000, a change that hit taxpayers in high-tax states particularly hard. With the potential for this limitation to change or expire, understanding how to navigate your state and local taxes becomes critical.

The increased property deductions and the elimination of the SALT cap can open the door for more itemized deductions on taxpayers’ returns. This change can significantly impact your tax strategy, allowing you to maximize your deductions and reduce your overall tax burden. By combining various itemized deductions, such as mortgage interest, medical expenses, and charitable contributions, you can further enhance your tax savings. For example, significant medical expenses that exceed 7.5% of your adjusted gross income (AGI) or substantial charitable contributions can add up, making itemizing more advantageous than taking the standard deduction.

One strategy is to review and possibly adjust where your income is generated, exploring avenues like real estate investments or business operations in states with lower tax rates. Additionally, staying informed on legislative changes at the state level can help you anticipate and plan for any adjustments in your tax planning strategy. By strategically timing your deductions, such as bunching charitable contributions into one tax year, you can take full advantage of the available deductions and minimize your tax liability.

Qualified Business Income (QBI)

For small business owners and self-employed individuals, the TCJA’s QBI deduction offers a deduction of up to 20% of qualified business income from pass-through entities. As we approach the TCJA expiration, maximizing this deduction can lead to significant tax savings.

Strategic planning, such as adjusting your business structure or income to qualify for the maximum deduction, can enhance your tax position. It’s essential to work closely with a tax professional to ensure compliance and to optimize this benefit fully.

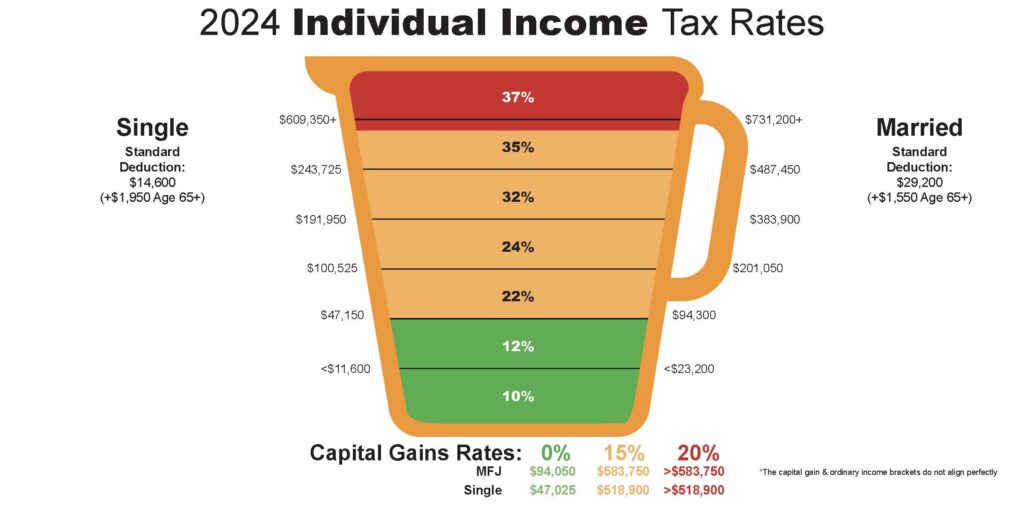

Tax Bracket Changes

With the potential for tax bracket adjustments post-TCJA, understanding how to navigate your income and investments to remain in a favorable tax bracket is key. Strategies might include timing the realization of capital gains, managing retirement distributions, or employing charitable giving strategies to manage your taxable income.

Anticipating changes and planning accordingly can help mitigate the impact of tax bracket shifts on your overall tax liability, ensuring that you’re positioned as advantageously as possible regardless of how the tax landscape evolves.

Conclusion

The expiration of the Tax Cuts and Jobs Act (TCJA) presents both challenges and opportunities for tax planning. By employing strategies like Roth conversions, taking advantage of federal gift and estate tax exemptions, optimizing SALT deductions, maximizing the QBI deduction, and strategically planning for potential tax bracket changes, you can position yourself to navigate the post-TCJA world with confidence.

As highlighted in the C2P Enterprises guide, the upcoming changes to the tax law are significant and demand proactive planning.

Don’t wait for the tax landscape to change before you act. Start planning now to take advantage of these strategies and minimize your future tax liabilities. Visit TheLynchFinancialGroup.com for more insights and guidance on financial planning and tax strategies or schedule a meeting with one of our advisors. Together, we can turn the challenges of tomorrow into the successes of today.